War, Energy and AI Datacenters

Australian Datacenter Viability in the 2026 Energy Shock

The convergence of systemic geopolitical conflict in West Asia and the unprecedented scaling of artificial intelligence infrastructure has created a profound structural paradox for the Australian economy. As of March 2026, the global energy landscape is defined by the "Operation Epic Fury" conflict in Iran, an event that has precipitated the most severe supply disruption in the history of the global oil and gas markets. For Australia, a nation currently attempting to position itself as a premier global hub for AI and hyperscale computing, this energy shock represents a critical stress test for the viability of massive capital projects currently under construction.

The 2026 Geopolitical Inflection Point and Global Energy Shock

The onset of hostilities involving Iran, the United States, and Israel in late February 2026 initiated a series of events that the International Energy Agency (IEA) has characterised as the greatest global energy and food security challenge in history. Unlike previous regional skirmishes, the 2026 conflict saw the immediate targeting of critical energy infrastructure and the weaponisation of maritime chokepoints.

The strategic blockade of the Strait of Hormuz serves as the primary driver of current global price volatility. This 29-nautical-mile waterway is the artery through which 20 million barrels of oil and 112 billion cubic metres of liquefied natural gas (LNG) pass annually. By 12 March 2026, the effective cessation of traffic through the Strait resulted in a production drop of approximately 10 million barrels per day from Kuwait, Iraq, Saudi Arabia, and the United Arab Emirates.

Commercial vessels have been forced to abandon the Suez Canal and Bab al-Mandab routes, opting instead for the much longer journey around the Cape of Good Hope to reach the Indian Ocean. This rerouting has added weeks to transit times and increased fuel consumption at a moment when kerosene-based products like diesel and jet fuel have more than doubled in price. Simultaneously, the targeting of the Ras Laffan industrial complex in Qatar by Iranian drone strikes on 1 March 2026 removed 20 per cent of the global LNG supply capacity in a single stroke.

Australian Energy Market Interdependencies and Vulnerabilities

Despite being one of the world's largest LNG exporters, Australia is uniquely exposed to global price shocks due to the integration of its domestic gas market with international export parity pricing. The National Electricity Market (NEM) relies heavily on gas-fired generation for "firming," providing essential power when renewable output fluctuates or when coal-fired plants, which are closing at an accelerated rate, go offline.

Because Australian domestic users effectively compete with Japanese and Korean buyers, the price spikes in Asia immediately flow through to Australian industry and households. By early March 2026, although the Australian government had implemented a $12/GJ pricing mechanism, the sheer scale of the global disruption threatened to force domestic prices higher as existing contracts expired. The forward electricity market began to reflect high volatility as the war progressed into March. New South Wales and Queensland regions showed high forward price sensitivity, while South Australia and Victoria remained moderate due to renewable penetration.

The AI Datacenter Landscape in Australia: 2026 Status Report

The Australian AI datacenter market reached a valuation of $1.78 billion in 2025 and is projected to grow to $2.13 billion in 2026, representing a Compound Annual Growth Rate (CAGR) of 19.65 per cent. This growth is fuelled by a transition from traditional CPU-based cloud computing to high-density GPU clusters required for Large Language Model (LLM) training and inference.

Several landmark projects represent billions in capital expenditure (CAPEX) and are designed to support rack densities that far exceed legacy standards:

NEXTDC S7 (Eastern Creek, Sydney): A planned 550MW+ hyperscale AI campus. In December 2025, NEXTDC signed a Memorandum of Understanding (MoU) with OpenAI to anchor this site as a GPU Supercluster. Total site investment reaches an estimated $7 billion.

Microsoft Australia Expansion: Microsoft has committed roughly $5 billion to $7.8 billion to add 20,000 GPUs across Sydney and Melbourne.

AirTrunk MEL2 (Melbourne): A 354MW hyperscale campus representing over $5 billion in investment. Total planned investment in Victoria is expected to exceed $7 billion.

Goodman Atlas (Sydney): A 500MW project in Sydney’s western growth corridor, part of a strategy to secure massive power allocations before grid capacity is exhausted.

Technical Evolution and Operational Viability

AI workloads have fundamentally changed datacenter engineering. Legacy facilities typically supported 5kW to 10kW per rack, whereas 2026-period AI facilities are being designed for 40kW to 60kW as a standard, with high-end liquid-cooled configurations pushing toward 100kW per rack.

The shift to liquid cooling is no longer optional. This technical necessity increases the electrical construction portion of the budget to approximately 55.7 per cent of total build costs. Furthermore, AI-optimised sites require 35-40 per cent of their budget for power infrastructure alone.

The spike in global energy prices directly threatens the Internal Rate of Return (IRR) for these massive projects. Electricity typically accounts for 40 per cent to 60 per cent of ongoing operating expenses (OPEX). A 40 per cent to 50 per cent increase in wholesale electricity prices can evaporate profit margins if not passed through to customers. Unlike traditional storage, GPU clusters for AI training run at 80 per cent to 90 per cent utilisation, meaning there is very little idle time to take advantage of off-peak pricing.

Regulatory Headwinds and the Social License to Operate

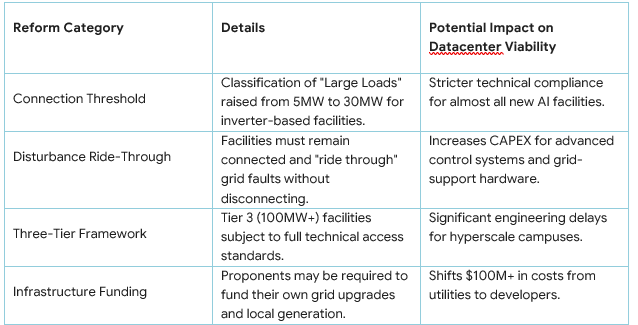

The 2026 energy crisis has intensified public and regulatory scrutiny of the datacenter industry. In March 2026, the Australian Energy Market Commission (AEMC) proposed reforms aimed at ensuring datacenters do not destabilise the grid or unfairly drive up costs for residents.

The AEMC has noted that most datacenters use inverter-based technology, which can suddenly disconnect during a voltage dip, increasing the risk of cascading outages. In response, Microsoft launched its "Community-First AI Infrastructure" initiative in early 2026, pledging that Microsoft’s datacenters will not increase residential electricity prices.

Kinetic Risks and the Shift to Australia

Perhaps the most startling development of the 2026 Iran war is the confirmation that hyperscale datacenters are now active military targets. On 1 March 2026, Iranian drones successfully targeted AWS facilities in the UAE and Bahrain, citing their role in supporting US military operations.

This kinetic shift has profound implications for Australian datacenter viability. The Middle East AI build-out has halted as the region is deemed too risky. This has led to a flight to safety, with capital being redirected to Australia, a "Five Eyes" nation with lower physical risk and a robust legal framework. The partnership between NEXTDC and OpenAI for the S7 site specifically highlights Australia's status as a secure location for sovereign compute capacity.

Strategic Synthesis: The Future of Australian Hyperscale

The Australian AI datacenter sector is currently caught between the technological demand and the global energy crisis. The 2026 Iran war has proven that digital sovereignty cannot exist without energy sovereignty. The new model for 2026 and beyond requires direct energy integration, where operators become energy producers by integrating large-scale solar, wind, and battery storage (BESS) directly into their site plans.

To calculate the impact of energy price spikes on project viability, analysts utilize a modified Net Present Value (NPV) formula where the energy OPEX is modelled as a stochastic variable based on LNG export parity benchmarks. As energy costs double and risk premiums increase due to the Iran conflict, the NPV of projects with high grid dependence frequently falls below zero, necessitating the Joint Venture and Power Purchase Agreement (PPA) strategies observed in the current market.

The long-term productivity potential of AI remains intact, but its trajectory is now inextricably linked to the reopening of the Strait of Hormuz and the cessation of hostilities. With that in mind, those who can avert the power crunch of 2026 will likely lead the next decade of digital growth - meaning that baseload power such as Coal and Nuclear with their unique energy density characteristics when compared to ‘renewables’ are once again poised to take the lead in the energy mix in Australia.

References

1. Geopolitical Volatility and the Sovereign AI Imperative: Assessing Australian Datacenter Viability Amidst the 2026 Energy Crisis.

2. The convergence of systemic geopolitical conflict in West Asia and the unprecedented scaling of artificial intelligence infrastructure.

3. Operation Epic Fury conflict in Iran and severe supply disruption.

4. Strait of Hormuz closure and global oil/LNG transit.

5. Qatar Ras Laffan drone strikes and LNG supply.

6. Australian energy market interdependencies and NEM vulnerabilities.

7. Australian AI datacenter market valuation and growth.

8. Major project details: NEXTDC, Microsoft, AirTrunk, Goodman.

9. Technical shifts in power density and cooling.

10. Financial impacts of energy price spikes and OPEX inflation.

11. Regulatory reforms (AEMC) and Community-First strategies.

12. Kinetic risks and Australia as a Five Eyes sanctuary.

13. Strategic synthesis and energy sovereignty.